US WEALTH INEQUALITY

- About Us

- Publications

- For Teachers

& Students - Working with

Communities - Supervising

Banks - Research &

Databases - President’s

Outreach

U.S. Wealth Inequality: Gaps Remain Despite Widespread Wealth Gains

February 07, 2024

By Ana Hernández Kent , Lowell R. Ricketts

Wealth—what a family owns less what they owe—is distributed unequally in the United States. Why does wealth matter? Wealth is important for upward economic mobility, allowing families to invest in their futures and their children’s futures, and to deal with financial bumps in the road.

In this post, we update our popular wealth inequality blog post using the most recent data from the 2022 release of the Federal Reserve Board’s Survey of Consumer Finances. Respondents are from households including single people and couples with or without children.1 All dollar amounts in this analysis are adjusted for inflation to 2022 dollars.

Notable Trends in Wealth Inequality from 2019 to 2022

The Household Wealth Pie Grew by 25%

Wealth grew markedly for all groups, but some families—grouped by race and ethnicity, age, and education—saw steeper growth.

Low-Wealth Groups Had the Largest Percentage Gains

Black and Hispanic families, young families, and families with a GED or less than a high school diploma had larger percentage gains between 2019 and 2022 than their high-wealth counterparts.

Wealth Gaps in Total Dollars Expanded

Despite the large percentage gains of low-wealth groups, because these groups were starting from much smaller dollar amounts, the wealth gaps in total dollars expanded. This is because a larger percentage increase of a smaller number can translate into smaller gains in dollar terms. For example, 50% of $1 is 50 cents, but 10% of $10 is $1.

Nevertheless, wealth increases for low-wealth groups are positive trends, indicating that, in an absolute sense, these families may be more financially stable than they were in 2019.

The Degree of Wealth Inequality

What was the wealth distribution overall in 2022? The degree of inequality might surprise you.

Total household wealth was $139.1 trillion, and there were about 131 million families. How was wealth split among these families?

Let’s say total household wealth was a pie with 10 slices. If it was meant to feed 10 people, an equal distribution would be one slice per person. However, that’s not what happens. A small number of families hold most of the wealth, and many families have relatively little or no wealth at all, based on the most recent Survey of Consumer Finances data.

One person, representing the top 10% of families, gets almost three quarters of the pie. The next four people, representing the next 40% of families, get almost a quarter of the pie. The final five people, representing the bottom 50% of families—or 65.5 million families—share the crumbs, owning 2% of the total pie.

That was the state of U.S. wealth inequality in 2022, which you can see in the animated graphic below.

SOURCES: Federal Reserve Board’s 2022 Survey of Consumer Finances and authors’ calculations.

Overall Wealth Trends

- To be in the top 10%, a family needed $1.92 million or more (about $507,000 more than in 2019). Their average wealth was $7.73 million, up 17% from 2019.

- To be in the next 40%, a family needed at least $192,000 in wealth. Their average wealth was $644,000, up 35% from 2019.

- To be in the bottom 50% meant a family had less than $192,000 in wealth. Their average wealth was $46,000, up a sizable 80% from 2019. Despite this growth, these families owned just a tiny portion of the nation’s wealth. Of this group, some 9.9 million families (about 7.5% of families overall) had negative net worth, meaning they were in debt.

Demographics matter. White, Asian, and older families, and families with at least a bachelor’s degree were overrepresented in the top 10% of the distribution and underrepresented in the bottom 50%. Conversely, Black, Hispanic, and younger families, and families with less than a bachelor’s degree, were underrepresented in the top 10% of the distribution and overrepresented in the bottom 50%.

Racial and Ethnic Gaps Remain Large Despite Sizable Wealth Growth for All

The racial wealth gap is perhaps the most discussed of the demographic wealth gaps. Between 2019 and 2022, wealth grew a substantial amount for each racial or ethnic group.2 In fact, for white, Black and Hispanic families, median inflation-adjusted wealth was at all-time highs. Yet very large racial/ethnic gaps remained, with white and Asian families owning significantly more wealth than Black and Hispanic families. You can see some of the gaps in the animated graphics below.

White Families’ Wealth

- White families’ median wealth was $287,000, growing a record 29% from 2019.

- As a group, white families owned 85% of total household wealth but made up 66% of households.

In 2022, the dollar gaps between white families and Hispanic and Black families grew markedly. This is despite the fact that median wealth grew more in percentage terms for these nonwhite groups. In dollar terms, the gains between 2019 and 2022 were smaller than for white families.

Black-White Wealth Gap Grows in Dollar Terms Despite Median Wealth Highs

SOURCES: Federal Reserve Board’s 2022 Survey of Consumer Finances and authors’ calculations.

NOTES: The figure shows median wealth for Black and white families between 1989 and 2022. Wealth values are for the median family, which is the one in the 50th percentile of the wealth distribution. Dollar values are adjusted to 2022 dollars using the consumer price index for all urban consumers (CPI-U) and rounded to the nearest $1,000. The bars represent the median Black-white wealth gap.

Black Families’ Wealth

- Black families’ median wealth was $45,000 in 2022, growing 66% from 2019.

- As a group, Black families owned 2% of total household wealth despite making up 11% of households.

- Black families had 16 cents per dollar of white median wealth.

- The Black-white gap grew to $242,000—up $47,000 from 2019.

The gap between Black families and white families is rooted in historical practices and policies (like redlining) that systematically stripped wealth (PDF) from Black families and facilitated wealth building among white families. Because of continued barriers and the intergenerational nature of wealth, it is very difficult for individuals or families to overcome the gaps.

Hispanic-White Wealth Gap Grows in Dollar Terms Despite Median Wealth Highs

SOURCES: Federal Reserve Board’s 2022 Survey of Consumer Finances and authors’ calculations.

NOTES: The figure shows median wealth for Hispanic and white families between 1989 and 2022. Wealth values are for the median family, which is the one in the 50th percentile of the wealth distribution. Dollar values are adjusted to 2022 dollars using the consumer price index for all urban consumers (CPI-U) and rounded to the nearest $1,000. The bars represent the median Hispanic-white wealth gap.

Hispanic Families’ Wealth

- Hispanic families’ median wealth was $61,000 in 2022. It increased 38% from 2019.

- As a group, Hispanic families owned 4% of total household wealth but made up 14% of households.

- Hispanic families had 21 cents per dollar of white median wealth.

- The Hispanic-white gap expanded to $226,000—up $48,000 from 2019.

Asian Families’ Wealth

- Asian families’ median wealth was $553,000 in 2022.

- As a group, Asian families owned 7% of total household wealth yet made up 4% of households.

- Asian families had almost twice as much wealth as the typical, or median, white family.

2022 marked the first year we were able to look at Asian households’ wealth, so growth rates are not available. Our future work will explore the wealth of Asian families in greater detail.

Wealth Gap Between Younger and Older Families Widens Steadily

In 2022, inflation-adjusted median wealth reached all-time highs for younger and older families. Middle-aged families’ median wealth was not at a high (it peaked in 2007), but these families also experienced wealth gains between 2019 and 2022.

The people in these groups change over time. In 1989, the youngest group was primarily made up of younger baby boomer families. For the 2022 survey results, we sorted families into three groups:3

- Young: ages 20 to 39, roughly millennials and Gen Zers

- Middle-aged: ages 40 to 59, roughly Gen Xers

- Older: ages 60 to 79, roughly baby boomers

Between 2019 and 2022, median wealth grew most rapidly for younger families. In 2022:

- Younger families had $57,000 in median wealth, up a record 137% from 2019. Growth rates in previous survey years for younger families were at most 25%, so the most recent increase was highly unusual and very large.

- Middle-aged families had $236,000 in median wealth, up 22% from 2019.

- Older families had $404,000 in median wealth, a record 35% rise from 2019.

Wealth, like other financial outcomes, follows what is known as a “life cycle.” In short, individuals have little wealth when they are young but typically accumulate some by their retirement. However, as the figure shows, that relationship has become starker over time. Despite the growth between 2019 and 2022, the gap in dollar terms between younger and older families has grown, as can be seen in the animated graphic below. For example, in 2001, older families had $254,000 more wealth than younger families. By 2022, this gap had grown by $93,000 to $347,000.

Generational Gap in Median Wealth Grows in Dollar Terms

SOURCES: Federal Reserve Board’s 2022 Survey of Consumer Finances and authors’ calculations.

NOTES: The figure shows median wealth for families grouped by age between 1989 and 2022. The age of the survey respondent is used. Families are grouped as follows: young, ages 20-39; middle-aged, ages 40-59; and older, ages 60-79. Wealth values are for the median family, which is the one in the 50th percentile of the wealth distribution. Dollar values are adjusted to 2022 dollars using the consumer price index for all urban consumers (CPI-U) and rounded to the nearest $1,000. The bars show the median wealth gap between older and younger families.

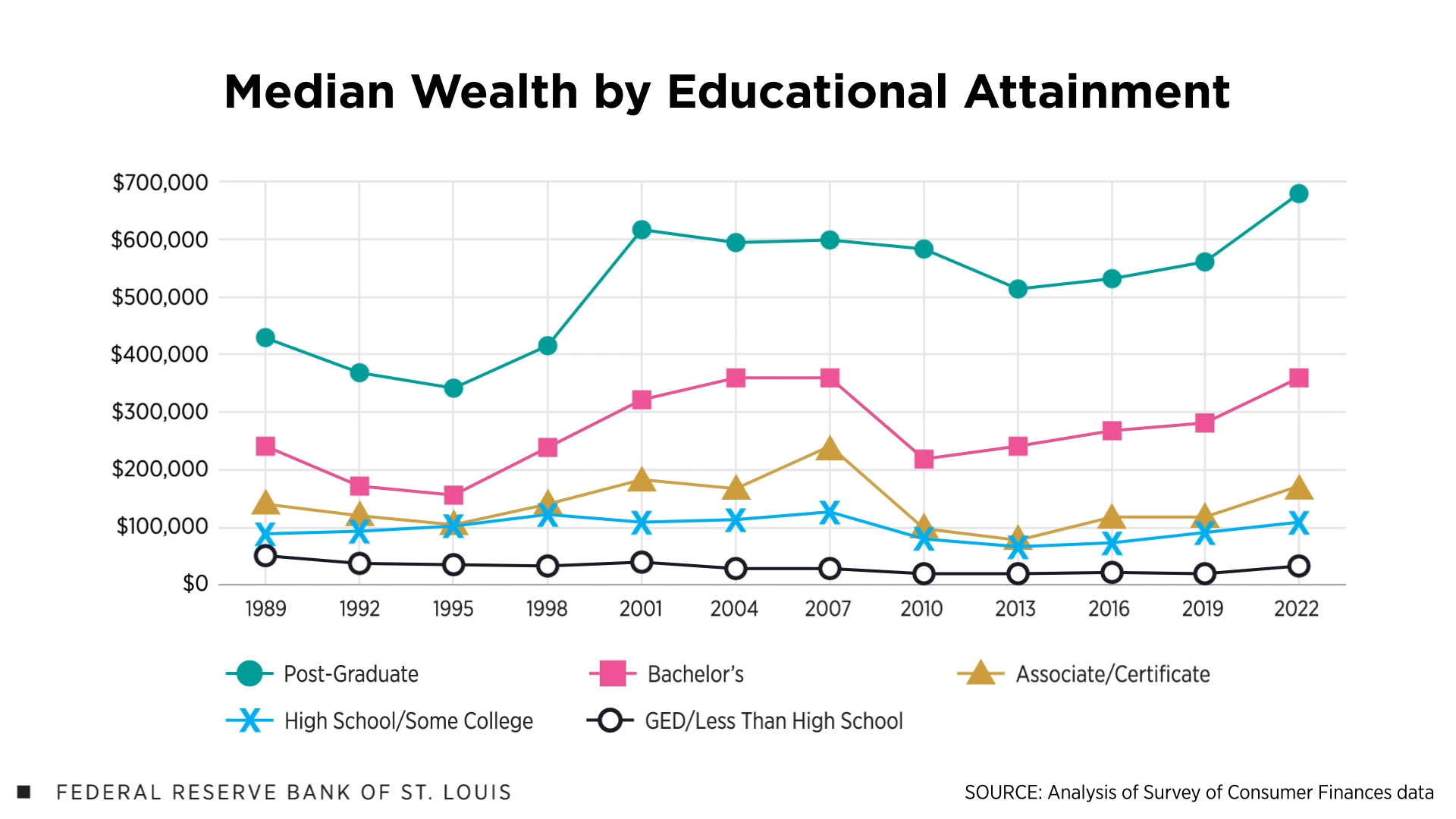

Wealth Grew the Most for the Least Educated, Counter to Previous Trends

In recent years, families whose respondent had at least a four-year college degree have experienced strong wealth accumulation. Together, they owned 77% of total wealth and made up 43% of all families in 2022.

Their median wealth was $459,000, up 28% from 2019. Families with less than a four-year degree had the same growth rate, but their median wealth was much lower at $98,000. Again, starting points matter: The absolute wealth gap between families with and without a bachelor’s degree widened an additional $78,000 to $361,000.

Wealth of Families with at Least a Bachelor’s Degree

- Family respondents with at most a bachelor’s degree had $359,000 in median wealth, growing 27% from 2019.

- Those with a postgraduate degree had $678,000 in median wealth, up 21% from 2019.

Wealth of Families with Less Than a Bachelor’s Degree

- Those with a GED, or with less than a high school diploma, had $34,000 in median wealth, up 67% from 2019. This was all the more notable because their wealth shrank by 8% between 2016 and 2019.

- Those with a high school degree, or some college but no degree, had $110,000 in median wealth, up 21% from 2019.

- Those with an associate degree or certificate had $171,000 in median wealth, up 45% from 2019.

The least educated families experienced the largest growth in percentage terms. This was a sharp contrast to the previous survey year (comparing 2016 to 2019), in which they were the only group whose wealth shrank. Nevertheless, the dollar gap between the most and least educated families grew.

The static figure below shows wealth gaps by educational level.

Median Wealth of Families with at Least a Bachelor’s Degree Is Much Higher Than for Others

SOURCES: Federal Reserve Board’s 2022 Survey of Consumer Finances and authors’ calculations.

NOTES: The figure shows median wealth for families grouped by education between 1989 and 2022. The educational attainment of the survey respondent is used. Wealth values are for the median family, which is the one in the 50th percentile of the wealth distribution. Dollar values are adjusted to 2022 dollars using the consumer price index for all urban consumers (CPI-U) and rounded to the nearest $1,000.

Takeaway: Widespread Growth Doesn’t Overcome Gaps

The period between 2019 and 2022 saw big gains in household wealth overall. White, Black and Hispanic families, younger and older families, and families with a postgraduate degree saw their wealth grow to record highs. Furthermore, families with historically lower wealth saw larger growth in percentage terms. Is this growth sustainable?

The rapid fiscal response to the COVID-19 pandemic played an important role in this growth through big liquid cash injection from programs like economic impact payment checks and the expanded child and dependent care tax credit. At the same time, the Federal Reserve engaged in parallel monetary policy to support financial stability. These collective efforts to address the economic effects of the pandemic partly contributed to robust financial and residential asset markets. However, many of these supports were intended to be limited in duration to the period of crisis and have since been discontinued. The path forward for asset markets (and family wealth) thus remains unknown.

Nevertheless, many low-wealth groups had more wealth in 2022 than in any previous survey year. These higher wealth levels may mean the typical family in these groups is better able to handle a downturn or invest in their futures. However, the growing dollar gaps between high-wealth and low-wealth families indicate that wealth inequality remains widespread.

Notes

- Estimates may differ from those in earlier articles due to inflation adjustment to 2022 dollars and changes in assignment of demographic characteristics for households. All demographic characteristics for the family were taken from the survey respondent, generally the most financially knowledgeable person.

- Families are grouped by the race and ethnicity of the survey respondent. We use data from responses to two questions on race and a separate question on ethnicity (added in 2004). Hispanics or Latinos may be of any race; we use the term Hispanics as a shorthand for this group. All other races are non-Hispanic, single-race (i.e., not multi-race). Asian Americans were added as a separate category in the 2022 public dataset. Thus, comparisons with earlier years are not available. While racial and ethnic groups are not monolithic, the data does not allow us to disaggregate them further.

- Families headed by those younger than 20 and 80 or older were not included in these analyses.

What Is the Survey of Consumer Finances?

The Federal Reserve Board’s Survey of Consumer Finances (SCF) is considered the gold standard on wealth data in the United States. The modern SCF began in 1989 and is conducted every three years, most recently in 2022. It allows researchers to explore the finances of specific groups—for example, “millennial, college-educated Black families”—with detail that would not be possible in other datasets.

The Federal Reserve Board’s Bulletin (PDF) also summarizes changes between the 2019 and 2022 surveys. Our estimates may differ slightly due to accessing the public versus private datasets and slight variation in demographic definitions.

See our team’s other report, The State of U.S. Wealth Inequality, for high-level wealth trends that are updated quarterly.

About the Authors

Ana Hernández Kent

Ana Hernández Kent is a senior researcher with the Institute for Economic Equity at the Federal Reserve Bank of St. Louis. Her research interests include economic disparities and the role of systemic biases and historical factors in wealth outcomes. Read more about Ana’s research.

Lowell R. Ricketts

Lowell R. Ricketts is a data scientist for the Institute for Economic Equity at the Federal Reserve Bank of St. Louis. His research has covered topics including the racial wealth divide, growth in consumer debt, and the uneven financial returns on college educations. Read more about Lowell’s research.

Related Topics

This blog explains everyday economics and the Fed, while also spotlighting St. Louis Fed people and programs. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

FOLLOW US

SIGN UP FOR EMAIL ALERTS

Receive updates in your inbox as soon as new content is published.

QUICK LINKS